26th Director's Report

To The Members,

Your directors are pleased to present the Twenty Sixth Annual Report of your Company with the audited accounts for the year ended March 31, 2012.

Financial Results

(in crores)

| For the year ended March 31, 2012 | For the year ended March 31, 2011 | |

|---|---|---|

| Profit Before Tax | 162.76 | 125.57 |

| Provision for Tax (Net of deferred tax) | 42.42 | 34.06 |

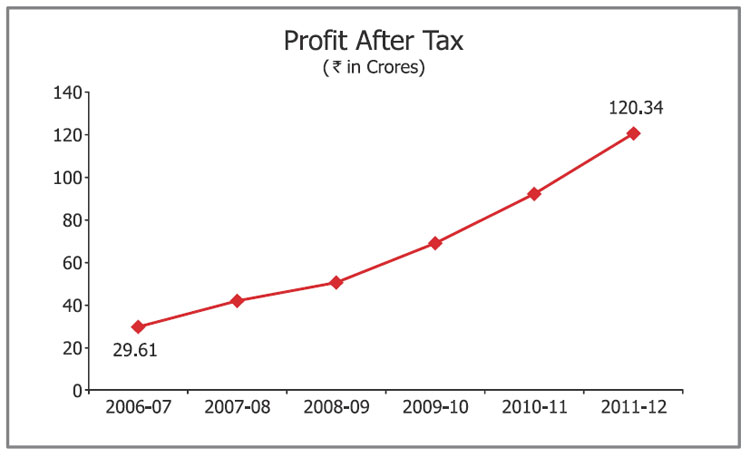

| Profit After Tax | 120.34 | 91.51 |

| Add: | ||

| Balance brought forward from last year | 61.15 | 45.88 |

| Amount Available for Appropriation | 181.49 | 137.39 |

| Appropriations: | ||

| Special Reserve | 28.00 | 22.00 |

| General Reserve | 15.00 | 9.20 |

| Additional Reserve u/s 29C of NHB Act, 1987 | 7.50 | 0.00 |

| Proposed Dividend | 40.60 | 38.67 |

| Additional Tax on Proposed Dividend | 6.59 | 6.28 |

| Dividend pertaining to previous year paid during the year | 0.10 | 0.09 |

| Balance Carried to Balance Sheet | 83.70 | 61.15 |

| 181.49 | 137.39 | |

Dividend

Your directors recommend payment of dividend of 11.50 per share of face value of 10 each for the year ended March 31, 2012 against a dividend of 11 per share (including a special dividend of 2.50 per share to commemorate the Company’s Silver Jubilee year) of face value of 10 each for the previous year. The dividend payout ratio for the year, inclusive of additional tax on dividend will be 39%.

Sub Division of Shares

Your directors have approved the sub-division of the nominal face value of the equity shares of the Company from 10 per equity share to 2 per equity share, subject to the approval of the members at the 26th Annual General Meeting (AGM) of the Company. The requisite resolutions for approval of the members have been set out in the notice convening the AGM.

- Graph: Profit After Tax

Disbursements

Loan disbursements during the year were 1,486.52 crores as against 1,210.69 crores in the previous year. GRUH continued to focus mainly on the retail segment and disbursed 1,295.59 crores to 21,586 families. Cumulative disbursements as at March 31, 2012 were 7,342.39 crores.

Golden Jubilee Rural Housing Finance Scheme

GRUH disbursed 528.03 crores in respect of 10,126 dwelling units during the year under the Golden Jubilee Rural Housing Finance Scheme of the Government of India. Cumulative disbursements under the scheme were 2,502.64 crores in respect of 79,219 dwelling units.

Rural Housing Fund

The National Housing Bank (NHB) has formulated a scheme called the Rural Housing Fund – 2008 (RHF). The scheme is aimed towards rural housing undertaken by families falling under the weaker section category as defined in the RBI guidelines on lending to the priority sector. During the year, GRUH has claimed 162.08 crores covering 3,922 families under this scheme. Cumulative disbursements under this scheme were 663 crores to 18,502 families.

Loan Assets

As at March 31, 2012, the loan assets increased to 4,077.43 crores with a growth of 28%. Loan assets in respect of retail segment also grew by 27% and stood at 3,901.25 crores.

- Graph: Loan Assets Profile

Non-Performing Loans

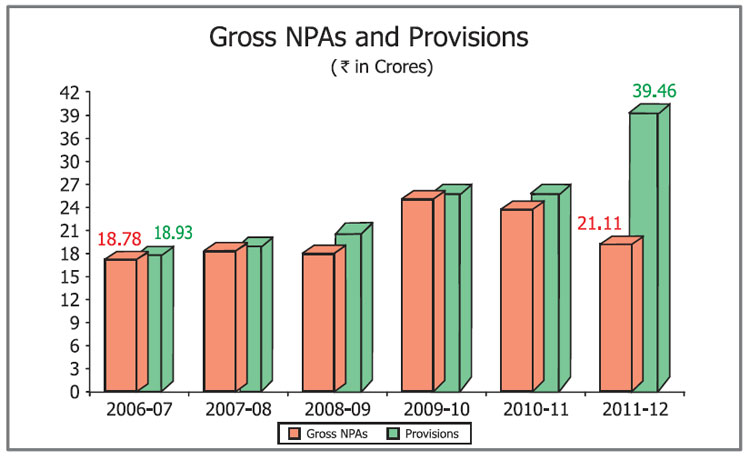

As per the prudential norms of NHB, GRUH’s Non-Performing Loans stood at 21.11 crores as at March 31, 2012 constituting 0.52% of the total outstanding loans of 4,077.43 crores. The Non-Performing Loans at the end of the previous year were 25.86 crores, constituting 0.81% of the total outstanding loans of 3,176.85 crores.

GRUH is required to carry a provision of 7.18 crores towards Non-Performing Loans as at March 31, 2012 as per the norms of NHB. However, as a measure of caution, GRUH carries a provision of 21.12 crores. Net Non-Performing Loans of GRUH was “NIL” on the outstanding loans of 4,077.43 crores as at March 31, 2012.

During the year, GRUH has written off 1.39 crores in respect of individual loans where the recovery was difficult in the near future. However, GRUH continued the recovery efforts in respect of written off loans of earlier years and could effect recoveries of 5.85 crores during the year in respect of such written off loans. GRUH also took possession of properties of the defaulting borrowers under the SARFAESI Act and has sold few of such acquired properties.

- Graph: Gross NPAs & Provisions

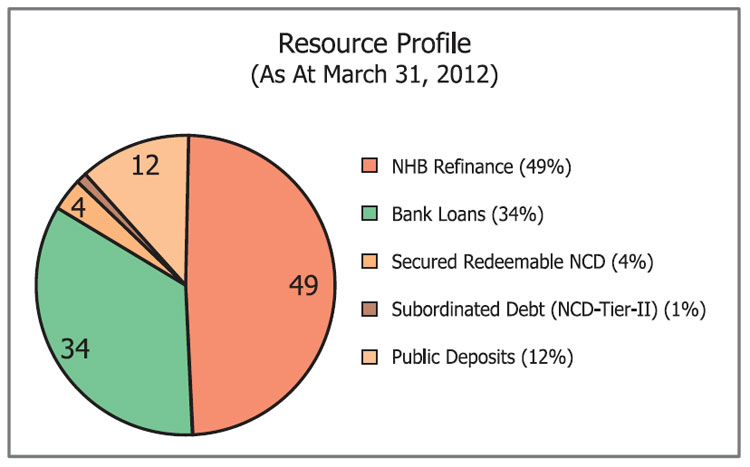

NHB Refinance

GRUH received refinance sanction of 1,450 crores from NHB during the year. GRUH availed refinance aggregating to 1,201.44 crores including 162.08 crores under RHF. The refinance outstanding as at March 31, 2012 was 1,893.34 crores.

Bank Term Loans

GRUH received sanctions from banks amounting to 2,225 crores of which GRUH availed loans aggregating to 1,575 crores. The outstanding bank term loans as at March 31, 2012 were 1,302.50 crores.

Subordinated Debt

GRUH did not issue any subordinated debt during the year. As at March 31, 2012, GRUH’s outstanding subordinated debt stood at 40 crores. The debt is subordinated to present and future senior indebtedness of the company and has been assigned rating of “ICRA AA+” by ICRA Limited (ICRA), indicating high safety with regard to timely payment of interest and principal. This rating carries a stable outlook. Based on the balance term to maturity, as at March 31, 2012, Nil of the book value of subordinated debt is considered as Tier – II capital under the guidelines issued by NHB for the purpose of computation of Capital Adequacy Ratio.

Non-Convertible Debentures (NCDs)

During the year, GRUH raised NCDs of 141.70 crores on private placement basis. The NCDs are rated “ICRA AA+” by ICRA, indicating high safety with regard to timely payment of interest and principal. This rating carries a stable outlook. The outstanding NCDs as at March 31, 2012 were 141.70 crores.

Commercial Paper

GRUH raised 2,240 crores through issuance of commercial paper during the year. GRUH’s commercial paper is rated “CRISIL A1+” by CRISIL Limited (CRISIL), indicating high safety as regards repayment. This rating carries a stable outlook. As at March 31, 2012, outstanding commercial paper was Nil.

Deposits

GRUH mobilised deposits of 324.65 crores and experienced a renewal ratio of 48.14% during the year. The outstanding balance of deposits as at March 31, 2012 was 455.46 crores. The rating assigned to GRUH’s deposit programme has been maintained by the two rating agencies viz. ICRA and CRISIL. GRUH’s deposits are rated “MAA+” and “FAA+” by ICRA and CRISIL respectively and both the ratings indicate high safety as regards timely repayment of principal and interest. These ratings carry a stable outlook.

Unclaimed Deposits

As at March 31, 2012, public deposits amounting to 3.75 crores had not been claimed by 872 depositors. Depositors were intimated regarding the maturity of deposits with a request to either renew or claim their deposits and subsequent reminders have been sent.

As per the provisions of Section 205C of the Companies Act, 1956, deposits remaining unclaimed and unpaid for a period of seven years from the date they became due for payment are required to be credited to Investor Education and Protection Fund (IEPF) established by the Government of India. In terms of Section 205C of the Companies Act, 1956, no claim would lie against the Company or the said fund after the said transfer. Accordingly, an amount of 5.24 lacs was transferred to the IEPF during the year.

- Graph: Resource Profile

Unclaimed Dividends

As at March 31, 2012, dividend amounting to 62.96 lacs has not been claimed by shareholders. GRUH has been intimating the shareholders to lodge their claim for dividend from time to time.

As per the provisions of Section 205C of the Companies Act, 1956, dividends remaining unclaimed for a period of seven years from the date of transfer to the unpaid dividend account are required to be credited to the IEPF. Accordingly, unclaimed dividend amount of 3.73 lacs in respect of the financial year 2003 -2004 was transferred to IEPF during the year. Unclaimed dividend amounting to 4.06 lacs in respect of the financial year 2004-2005 is due for transfer to IEPF in July 2012. In terms of Section 205C of the Companies Act, 1956, no claim would lie against the Company or the said fund after the said transfer.

Dematerialisation of Shares

As at March 31, 2012, 97.59% of equity shares of GRUH have been dematerialised by shareholders through National Securities Depository Limited and Central Depository Services (India) Limited.

Pursuant to an amendment to Clause 5A of the Listing Agreements, the Company affirms that there are no share certificates issued to its shareholders in physical form which are lying unclaimed.

Risk Management Framework

The Company has a Risk Management Framework, which provides the mechanism for risk assessment and mitigation. The Risk Management Committee (RMC) of the Company comprises the Managing Director, the Executive Director and some members of senior management.

During the year, the RMC reviewed the risks associated with the business of the Company, its root causes and the efficacy of the measures taken to mitigate the same. Thereafter, the Audit Committee and the Board of Directors also reviewed the key risks associated with the business of the Company, the procedures adopted to assess the risks, efficacy and mitigation measures.

Investments

GRUH continues to maintain its Statutory Liquid Ratio (SLR) as stipulated by NHB. Accordingly, GRUH carried investments in approved securities aggregating to 45.30 crores as at March 31, 2012 to meet the requirement of the SLR. GRUH has classified its investments as long-term and valued them at cost. Adequate provision, towards loss, if any, to be experienced on redemption of investments on maturity has been made.

- Graph: Capital Adequacy Ratio

Regulatory Guidelines

NHB has introduced provisioning on standard individual home loans during the year. NHB has stipulated a rate of provisioning of 0.40% on standard home loans. NHB has also enhanced the requirement of provisioning on standard non-residential property loans from 0.40% to 1.00%. As a result, GRUH is required to carry a provision of 14.81 crores on standard individual home loans of 3,703.70 crores and a provision of 3.53 crores on standard non-residential property loans of 352.62 crores as at March 31, 2012. GRUH has utilised an amount of 7.80 crores (net of deferred tax of 3.74 crores) from General Reserve in respect of the standard individual home loans at the beginning of financial year of 2,884.53 crores.

NHB also enhanced the provisioning requirement in respect of non-performing loans on sub-standard loan from 10% to 15% and on bad & doubtful loans from the band of 20% – 50% to the band of 25%-100%.

NHB has directed housing finance companies (HFCs) to not levy prepayment fee on preclosure of housing loans with effect from October 19, 2011.

NHB has also directed HFCs to apply uniform rate of interest to the old and new home loan customers who have similar risk profiles. This direction is to be implemented in the financial year 2012-13.

GRUH has complied with these regulatory changes as directed by NHB.

GRUH continues to comply with the guidelines issued by NHB regarding accounting standards, prudential norms for asset classification, income recognition, provisioning, capital adequacy, concentration of credit, credit rating, ‘Know Your Customer’ – (KYC), fair practices code and real estate & capital market exposures. The details of compliances are outlined in the Management Discussion and Analysis Report.

The National Housing Bank Act, 1987, empowers NHB to levy a penalty on Housing Finance Companies for contravention of the Act or any of its provisions. NHB has not levied any penalty on GRUH during the year.

The task of overseeing the implementation of the Asset Liability Management (ALM) has been entrusted to the Audit Committee which oversees and reviews the ALM position vis-à-vis risk management.

GRUH’s Capital Adequacy Ratio stood at 13.95% as against the minimum requirement of 12%. Tier – I capital was 13.29% against the minimum requirement of 6%.

The Government of India has set up the Central Registry of Securitisation Asset Reconstruction and Security Interest of India (CERSAI) under section 21 of the SARFAESI Act 2002 to have a central database of all mortgages created by lending institutions. The object of this registry is to compile and maintain data relating to all transactions secured by mortgages. Accordingly, GRUH has registered with CERSAI and submitted data in respect of all outstanding loans as at March 31, 2012.

Human Resource Development

At GRUH, human resource development is considered vital for effective implementation of business plans. Constant endeavours are being made to offer professional growth opportunities and recognitions, apart from imparting training to employees. During the current year, besides the in-house induction training programmes in lending operations, recoveries and accounts, employees were also nominated to training programmes conducted by NHB and other institutions.

GRUH’s staff strength as at March 31, 2012 was 473.

Employees Stock Option Scheme

The stock options granted to directors and eligible employees operate under two schemes, i.e. ESOS-2007 and ESOS-2011. The disclosures as required under Clause 12.1 of the SEBI (Employee Stock Option Scheme and Employee Stock Purchase Scheme) guidelines, 1999, as amended, have been made in the annex to this report.

- Graph: Net Worth & Return on Net Worth

Particulars regarding Conservation of Energy, Technology Absorption andForeign Exchange Earnings and Expenditure

GRUH does not have any foreign exchange earnings and expenditure. Particulars relating to conservation of energy and technology absorption stipulated in the Companies (Disclosure of Particulars in the Report of the Board of Directors) Rules, 1988, are not applicable to GRUH.

Particulars of Employees

GRUH had 1 employee as at March 31, 2012 employed throughout the year who was in receipt of remuneration of ` 60 lacs or more per annum.

In accordance with the provisions of Section 217(2A) of the Companies Act, 1956, read with the Companies (Particulars of Employees) Rules, 1975, as amended, the name and other particulars of such employees are set out in the annex to the Directors’ Report. However, as per the provisions of Section 219(1) (b) (iv) of the Companies Act, 1956, the Directors’ Report is being sent to all shareholders of the Company excluding the annex. Any shareholder interested in obtaining a copy of the said annex may write to the company secretary at the registered office of the Company.

Directors

In accordance with Articles 134 and 135 of the Articles of Association of the Company and the provisions of the Companies Act, 1956, Mr. Prafull Anubhai and Mr. K. G. Krishnamurthy, directors of the Company, retire by rotation at the ensuing Annual General Meeting (AGM) and are eligible for re-appointment. Your directors commend their re-appointment.

Necessary resolutions for the re-appointment of the aforesaid directors have been included in the notice convening the ensuing AGM.

All the directors of the Company have confirmed that they are not disqualified from being appointed as directors in terms of Section 274(1)(g) of the Companies Act, 1956.

Auditors

M/s. Sorab S. Engineer & Co., Chartered Accountants, statutory auditors of the Company having registration number 110417W retire at the ensuing AGM and are eligible for re-appointment.

The Company has received a certificate from the statutory auditors to the effect that their re-appointment, if made, would be within the limits prescribed under Section 224(1B) of the Companies Act, 1956. The statutory auditors have also confirmed that they hold a valid certificate issued by the “Peer Review Board” of The Institute of Chartered Accountants of India.

Corporate Governance – Voluntary Guidelines

The Board of Directors have taken cognisance of the ‘Corporate Governance Voluntary Guidelines 2009’ issued by the Ministry of Corporate Affairs (MCA) in December 2009. While the guidelines are recommendatory in nature, the board recognises the importance and need to constantly assess governance practices thereby ensuring a sustainable business environment that generates long-term value to all key stakeholders. The board has adopted several provisions of the said guidelines.

Directors’ Responsibility Statement

In accordance with the provisions of Section 217(2AA) of the Companies Act, 1956 and based on the information provided by the management, your directors state that:

- In the preparation of annual accounts, the applicable accounting standards have been followed;

- Accounting policies selected were applied consistently. Reasonable and prudent judgements and estimates were made so as to give a true and fair view of the state of affairs of the Company as at March 31, 2012 and of the profit of the Company for the year ended on that date;

- Proper and sufficient care has been taken for the maintenance of adequate accounting records in accordance with the provisions of the Companies Act, 1956 for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities;

- The annual accounts of the Company have been prepared on a going concern basis.

Management Discussion and Analysis Report

In accordance with clause 49 of the listing agreements, the Management Discussion and Analysis Report forms a part of this report.

Acknowledgements

Your directors take this opportunity to place on record their appreciation to all employees for their hard work, spirited efforts, dedication and loyalty to GRUH. The employees have worked based on principles of honesty, integrity and fair play and this has helped GRUH in maintaining its growth. The directors also wish to place on record their appreciation to shareholders, depositors, referral associates, NHB, financial institutions and banks for their continued support.

{kind=link}